PlattsWeekly Deep Dive 24.04.2026

Geopolitical fault line, demand collapse in China, and the reassembly of global flows

The current week resembles a chess game on three boards simultaneously: Washington and Tehran are negotiating a ceasefire in Pakistan, Beijing is “burning out” domestic demand with electric vehicles, and the largest traders are rewriting the planet’s logistics while the Strait of Hormuz remains closed. Platts has recorded extraordinary movements: from the collapse of differentials on Angolan crude to a record divergence of WTI and Brent.

Tectonic shift: WTI and Brent diverge in crisis On April 24, futures closed with an unprecedented divergence:

ICE Brent (June) rose by $0.26 to $105.33/bbl.

NYMEX WTI (June) fell by $1.45 to $94.40/bbl. The Brent-WTI spread widened to $10.93 — this is the maximum since the start of the conflict. For comparison: on April 17 it was $6.09, and before the war the average value was $4–$6.

Why is this happening?

Brent receives a geopolitical premium — fear of a breakdown of negotiations in Pakistan and the de facto naval blockade of Hormuz. On April 23, only 7 vessels passed through the strait (against 9 the day before). This is the third day with a single-digit number of transits — “a sign of slowing momentum,” according to S&P Global Commodities at Sea. The market sees that the “double control” of the US and Iran is being maintained.

WTI is experiencing internal pressure (see USA Block). The Brent/WTI spread at the level of $10.93 gives a powerful signal for the export of American oil — the arbitrage window to Europe is wide open. WTI FOB USGC is trading at $101.59/bbl with a premium of $9.97 to NYMEX WTI.

USA: Domestic overheating and export boom The States found themselves in a unique situation: the domestic market is suffering from a surplus of raw materials, while foreign markets are fighting for every barrel.

Strategic Petroleum Reserve (SPR) presses on WTI:

The US is actively releasing crude oil from the SPR. In the week to April 17 alone, SPR stocks decreased by 2.1 million barrels.

Two supertankers (2.1 million barrels each) with Bryan Mound sour grade (API 33.3, sulfur 1.44%) are already on their way to the Mediterranean. This grade competes directly with the former Urals, Kirkuk, and KEBCO, crashing their differentials.

In total, according to traders’ estimates, Mediterranean refineries have contracted more than 10 cargoes of 600–700 thousand barrels from the SPR.

Export boom:

American crude oil exports reached a seven-month high — 5.2 million b/d.

Main destinations: Netherlands (1.7 million b/d, sharp growth), South Korea (286 thousand b/d, decline). Re-export of Canadian Cold Lake to the Netherlands amounted to 222 thousand b/d.

The extension of the Jones Act Waiver for 90 days (from May 18) allows foreign tankers to transport petroleum products between US ports. This has already led to the first deliveries of gasoline and diesel from the USGC to the West Coast, which suffers from a deficit after the closure of Phillips 66 and Valero plants.

Refineries under pressure:

Marathon Carson (California): unscheduled flaring on April 23. The cause is being investigated, but the market reacted with an instant rise in CARB gasoline and diesel prices. Export from the main

BP Cherry Point (Washington): fire on April 18, four injured. The plant is on planned maintenance, status unclear. This is a key supplier of jet kerosene for the West Coast.

ExxonMobil Beaumont (Texas): unscheduled flaring on the FCCU on April 22, but the company stated it had fulfilled all contractual obligations.

Bottom line for the US: A surplus of oil from the SPR and high exports pressure WTI, creating a unique discount to Brent. But the domestic petroleum products market, especially on the West Coast, remains extremely tense due to logistical constraints and refinery accidents.

THE ARAB KNOT — Hormuz, sanctions, and the redistribution of flows The Middle East remains the epicenter of the crisis. Military actions and sanctions are redrawing the map of supplies.

Iran — double blockade:

The US has imposed a naval blockade on all Iranian ports, with 34 vessels stopped (per CENTCOM). Five VLCCs with 9 million barrels of Iranian oil have been seized (Majestic X, Tifani, Dorena, Hedy, Hero II).

The IRGC attacked three container ships (MSC Francesca, Epaminondas, Euphoria) on April 22. Of the 78 vessels that left Hormuz from April 13 to 21, 47 were linked to Iran. Transit has fallen to a minimum.

Exports from the main Kharg terminal have decreased from the usual 8 million barrels per week to 3 million. This is “either a temporary disruption or the first signs of sustained destruction of export infrastructure,” — Windward.

But Iranian oil on water has grown to 84.5 million barrels (from 73.7 million), which indicates the continuation of shadow operations (transshipment in Malaysia, “gray” logistics). US sanctions against Hengli Petrochemical and 38 vessels are aimed at breaking these chains.

Saudi Arabia and the UAE — defense and maneuver:

On April 7, ballistic missiles were aimed at the petrochemical hub of Jubail (60 million tons/year, 5% of world production). Intercepted, but debris fell near the facilities.

On April 5, a strike drone caused a fire at a Bapco Energies storage facility (Bahrain). Damage is being assessed.

Fujairah (UAE): middle distillate stocks grew by 13.7% over the week (to 1.14 million barrels), as exports are blocked. Vopak reports that 8% of the terminal’s capacity is not working due to the conflict. Demand for bunkering in Fujairah has fallen, shipowners are avoiding the region.

Kuwait resumed fuel oil deliveries to Singapore (34,999 tons) after a three-week break — the first signs of “seepage” through the blockade.

Iraq:

Iraq received a contract for drilling 17 wells at East Baghdad South (Chinese EBS), which speaks of long-term plans to ramp up capacity despite the war.

Redistribution of flows:

Arab producers are redirecting exports bypassing Hormuz. Saudi Arabia is increasing supplies through Yanbu (Red Sea) to Europe (125,000 tons of diesel in April).

Oman is sending rare consignments of jet fuel to Europe (Sea Penguin, 102,000 tons), the arbitrage is open.

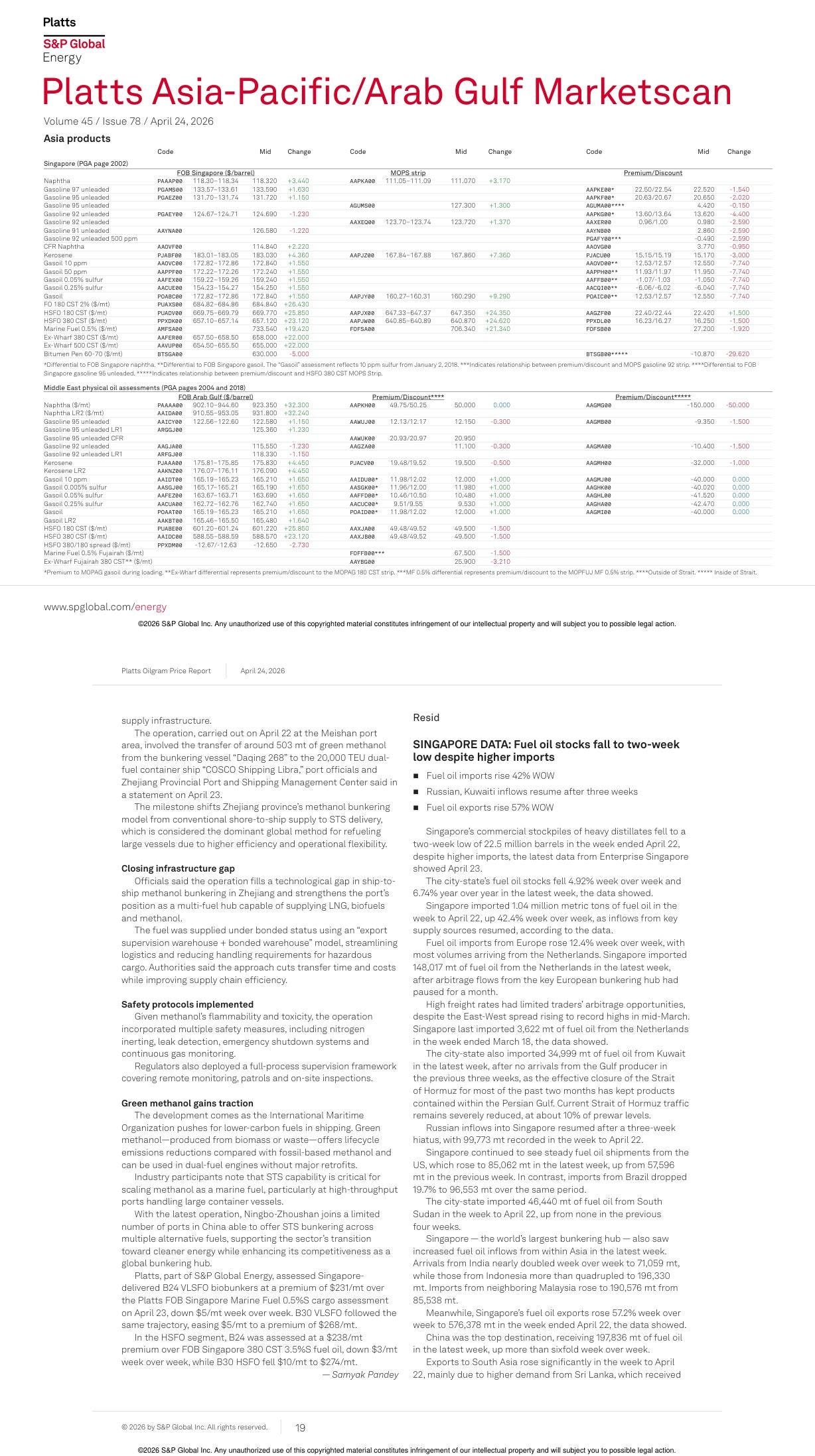

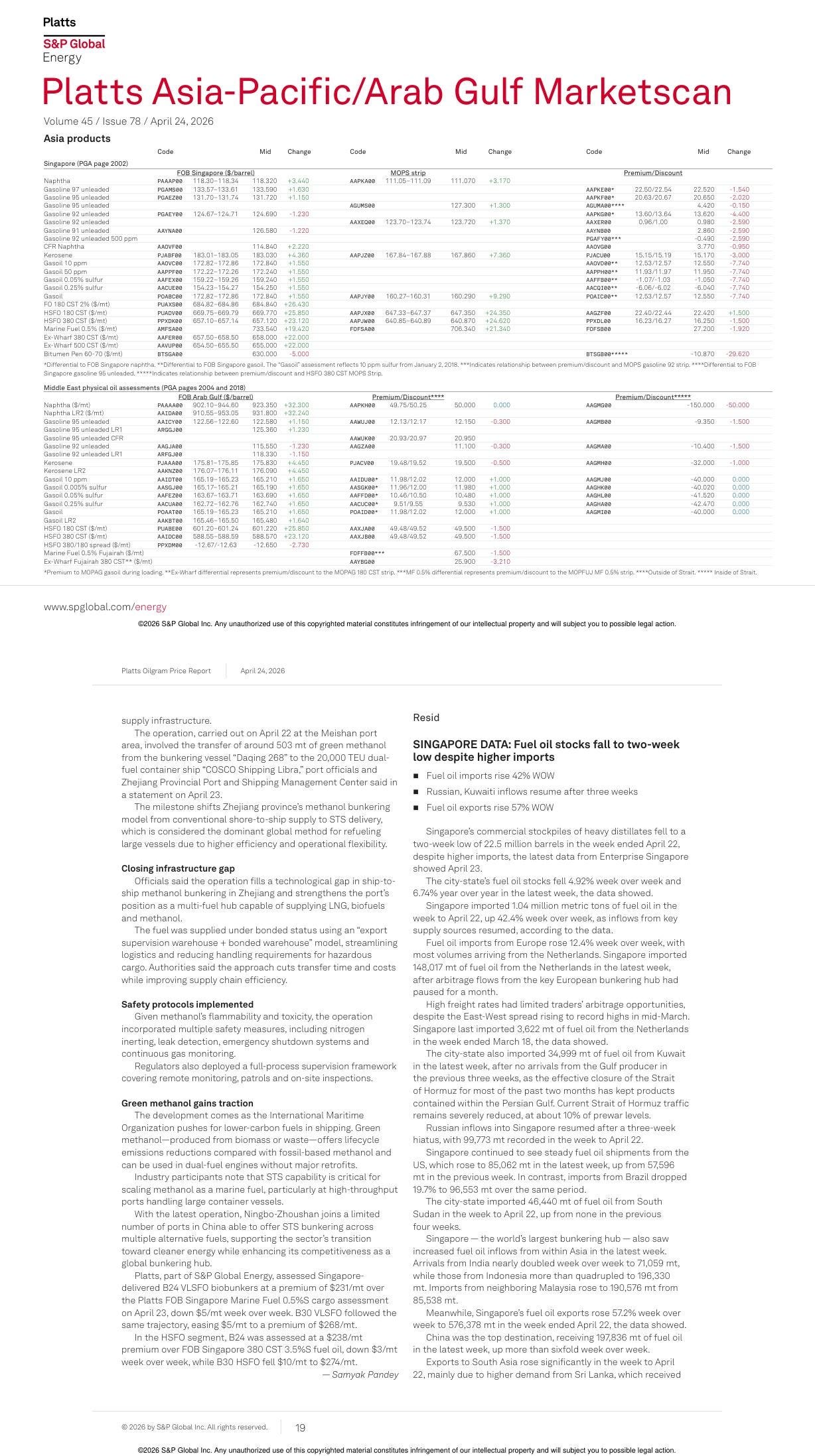

But total exports from the region remain critically low, which supports the premium on Middle East sour crude (Cash Dubai/Oman/Murban) at the level of $11.91 to futures — stability against the backdrop of the BFOE collapse.

ASIA OUTSIDE OF CHINA — who suffers, who wins Outside of China, an acute deficit is unfolding in Asia from emergency measures and unexpected opportunities.

India:

All refineries are operating at full capacity, raw material stocks are sufficient. Retail sales of gasoline and diesel grew by 13% in the first 21 days of April (Indian Oil Corp).

Diesel exports fell by 27% over the week (to 336 thousand tons), supplies to Singapore decreased. India is reorienting exports to Singapore, Australia, Bangladesh.

Indian Oil Corp and HPCL are actively seeking urgent crude oil supplies for June-July (tenders for 2 million barrels), including Murban with delivery to Fujairah.

Japan:

Emergency SPR release: from May 1, METI will release 5.8 million kiloliters (36.5 million barrels) from state reserves to ENEOS, Idemitsu, Cosmo Oil, Taiyo Oil. Cost: ¥540 billion ($3.4 billion). Pricing formula: February OSP of producer countries × Brent change (February-March).

Import diversification: Cosmo Oil will receive the first tanker with American WTI through the Panama Canal (loading March 22).

Canadian heavy grades (Cold Lake, AWB) are being actively studied as a replacement for Upper Zakum and Arab Heavy.

Mexico agreed to send “some volume” of oil to Japan (presidential agreement).

Stocks as of April 21: 214 days of consumption (131 state reserve, 81 private, 3 joint).

South Korea:

Historic agreement with Canada: KCS and the government of Alberta on April 20 signed a joint statement on simplified certification of oil origin. Now Cold Lake and AWB will be taxed at a 0% rate (instead of 3% under the FTA). This opens the door for imports of up to 33 million barrels/year. SK refineries are already in negotiations.

Jet fuel exports grew in March by 29.2% YoY to 7.35 million barrels, but decreased by 14.4% MoM. South Korea flooded the market with spot cargoes, crashing Asian premiums.

Gasoline stocks grew by 32.3% MoM, export restrictions and high prices pressure domestic demand.

Pakistan:

Attock Refinery halted the CDU due to a blockade of tanker traffic in Islamabad (foreign delegations expected for negotiations). Halt of feedstock supply and product shipments.

Fuel oil exports in March fell by 21% YoY (to 127,730 tons) — the government is using it for power generation due to LNG shortages (only 2 out of 8 scheduled cargoes arrived). Fuel oil consumption has doubled.

Indonesia:

Purchase of 150 million barrels of Russian oil through the end of 2026, supplies gradual due to limited storage.

Also looking for additional volumes in the US (Pertamina team is already there).

Consumption 1.6 million b/d, production only 0.6 million b/d — deficit is critical.

Singapore:

Middle distillate stocks grew by 4.38% to 10.72 million barrels (maximum since October 2025). Gasoil imports collapsed by 57% over the week, exports also fell.

Jet fuel imports from Brunei (20,908 tons) — first instance since 2021. Unusual flows: Singapore exported jet to Japan (37,739 tons), although Japan usually buys from Korea and China.

Sri Lanka:

Ceypetco purchased 8 thousand tons of jet A-1 and 32 thousand tons of 0.05% gasoil with delivery in late April from Trafigura. Premium $48/bbl to MOPS — extreme level. The government has switched to direct purchases outside standard procedures due to disruptions in supply chains.

Australia:

The government secured another 100 million liters of diesel (in addition to 300 million liters earlier). The fuel is being directed to Queensland (Townsville, Gladstone, Mackay).

Total volume of emergency spot purchases reached 400 million liters per week (Ampol, BP, Viva Energy).

Gasoline stocks grew to 46 days (higher than at the start of the conflict).

EUROPE — between the Russian turn and American salvation The European market is the arena for the clash of two forces: the return of Russian supplies and American dumping from the SPR.

Druzhba returns:

On April 23, Hungary and Slovakia received the first consignments of Russian oil via the southern branch of Druzhba after a three-month break. Planned deliveries through the end of April — 119 thousand tons. Slovnaft (MOL) resumed full loading of the Bratislava refinery.

This unblocked the 20th EU sanctions package against Russia, as well as a €90 billion loan to Kyiv. Hungary lifted its veto after a change of government.

But the northern branch of Druzhba is under threat: Kazakhstan reported the cessation of supplies to Germany for May (PCK Schwedt plant, ~17% of feedstock). This will hit eastern Germany and affect the Czech Republic.

The Czech Republic is preparing an emergency plan:

The Minister of Industry announced the preparation of an agreement with Slovakia (Slovnaft) on access to emergency stocks of gasoline and diesel.

Diversification is also underway: the PM’s visit to Kazakhstan and Azerbaijan on April 26, possible supplies from Algeria.

EU sanctions — 20th package:

The largest package of listings in two years: 120 new entities.

Ban on imports from the ports of Murmansk and Tuapse, as well as from the Karimun terminal (Indonesia) — a blow to the shadow fleet.

Ban on servicing Russian LNG tankers and icebreakers, from 2027 — on providing LNG terminals.

46 vessels sanctioned (total number — 632), mandatory due diligence introduced for the sale of tankers.

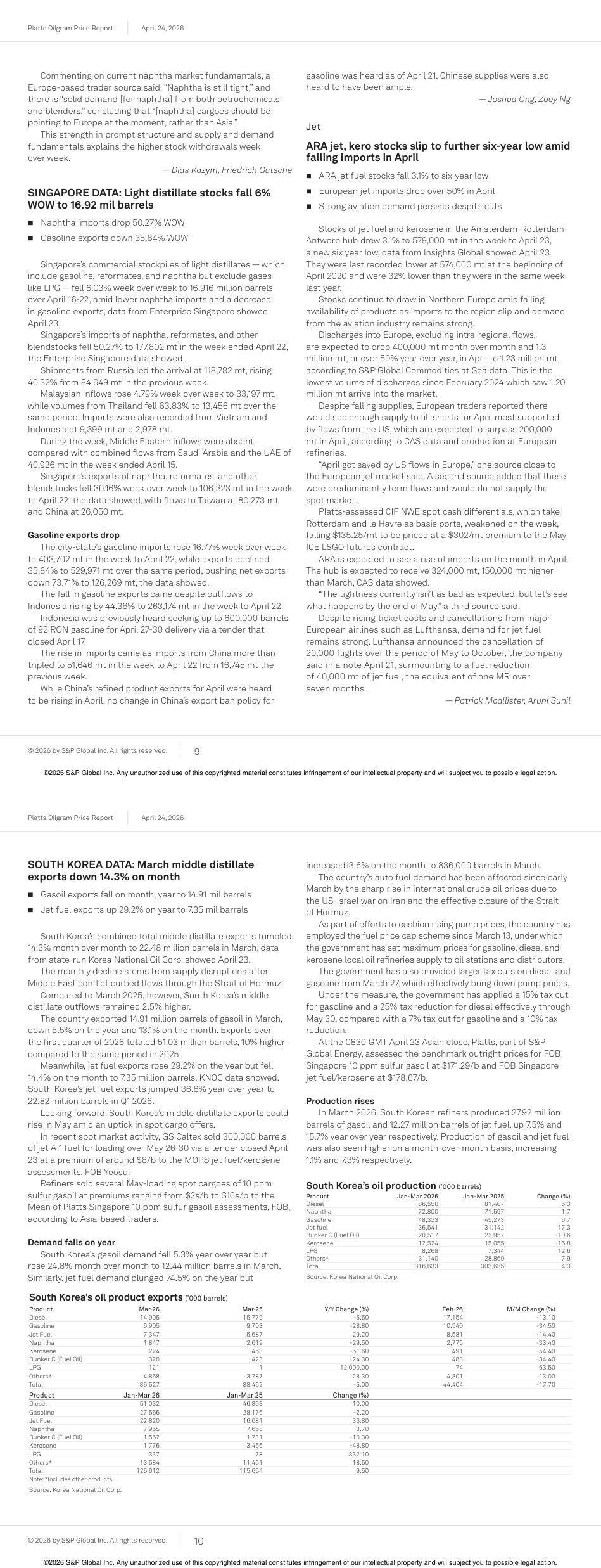

Mediterranean differentials are collapsing:

Azeri Light CIF Augusta fell by $1.72 in a day to $7.76/bbl to Dated Brent. Over the week, the loss amounted to more than $5.

CPC Blend fell by $0.585 to $3.02/bbl (offers went at $2.50 without interest).

Es Sider and Saharan Blend lost $1.50/bbl each. Offers on Saharan Blend fell from $10 to $3/bbl in one session.

Reason: refineries in the region contracted for the first half of May, demand collapsed.

LNG and power generation:

Antwerp recorded a collapse of LNG supplies from Qatar (-37%), but growth from Russia (+30%) and Nigeria (x2). American LNG doubled.

Pakistan and India switched to fuel oil due to LNG shortages, which creates additional demand for HSFO.

Warm weather kills gasoil demand:

Propane FCA ARA fell to a premium of $87/t to CIF ARA (minimum since September 2025). Heating is off, consumers are not lifting term volumes.

50 ppm and 0.1% gasoil in Europe are “needed by no one” — traders call it a blending component.

Rhine level at Kaub: 132 cm (falling). Not critical yet, but may limit barge supplies inland.

Jet kerosene: maximization and deficit:

All European refineries, according to the head of Shell Netherlands, have been switched to maximum jet fuel yield mode.

But possibilities are limited: “degrees of freedom — several percent,” — Frans Everts.

Lufthansa cancelled 20,000 flights (May-October), reducing consumption by 40,000 tons of jet fuel. But this will not save the market: ARA stocks are at a minimum, imports from Korea and Nigeria do not compensate for the lost volumes from the Persian Gulf.

Oil market:

Urals CIF Med trades at a discount of $18.50/bbl to Dated Brent (against $10-12 before the war).

Supplies from the port of Ust-Luga fell by 100,000 b/d after a drone attack. The Tuapse refinery (240,000 b/d) was halted after two strikes. The fire was extinguished only after 5 days. The leak of petroleum products into the Tuapse River continues.

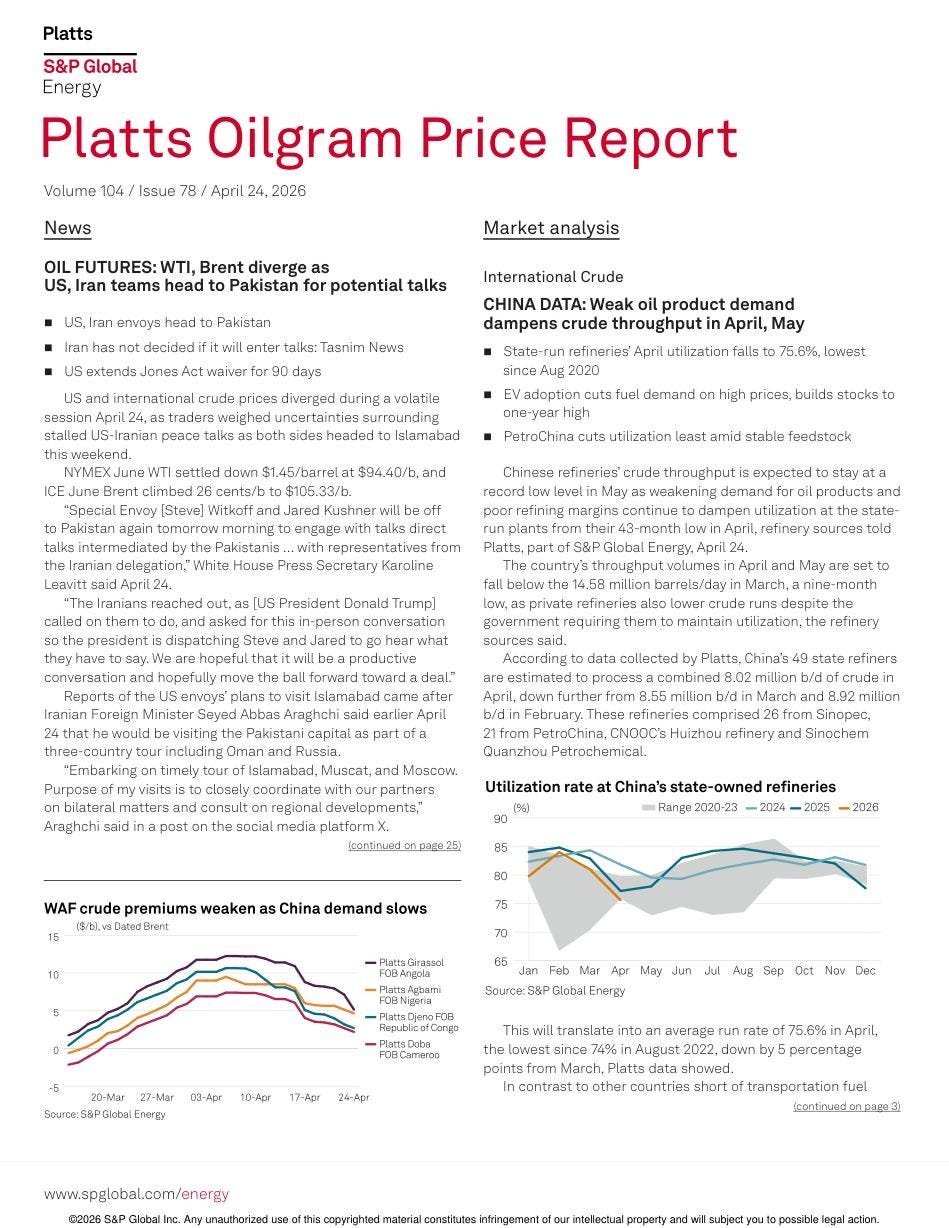

Demand collapse in China: how the EV revolution is killing oil demand Platts is publishing shocking figures on China:

Sinopec utilization fell to a 73-month minimum (70.9%), PetroChina — to 81%. Private refineries reduced refining to 81% (against 89% in March).

Gasoline stocks soared to an annual maximum (10.44 million tons) — 0.07 million tons above the previous peak of January 3, 2025. Diesel stocks reached a 56-week maximum of 13.64 million tons.

Retail fuel sales at Sinopec and PetroChina collapsed by 10-20% year-on-year due to high EV penetration and price increases.

The Chinese government is artificially restraining retail prices: for the period March 23 – April 21, the growth of retail prices for gasoline amounted to only 1,580 yuan/t ($27.20/bbl), for diesel — 1,515 yuan/t ($29.75/bbl), while according to the benchmark formula they should have grown by 3,005 and 2,890 yuan/t respectively. Moreover, the formula does not take into account freight and insurance, so refining has become unprofitable.

China has turned into a seller. According to Mercuria, the country is “aggressively selling” crude oil from accumulated stocks. Oil exports in March amounted to 170,000 b/d — maximum since January 2025. Chinese companies are re-offering West African cargoes back to Europe.

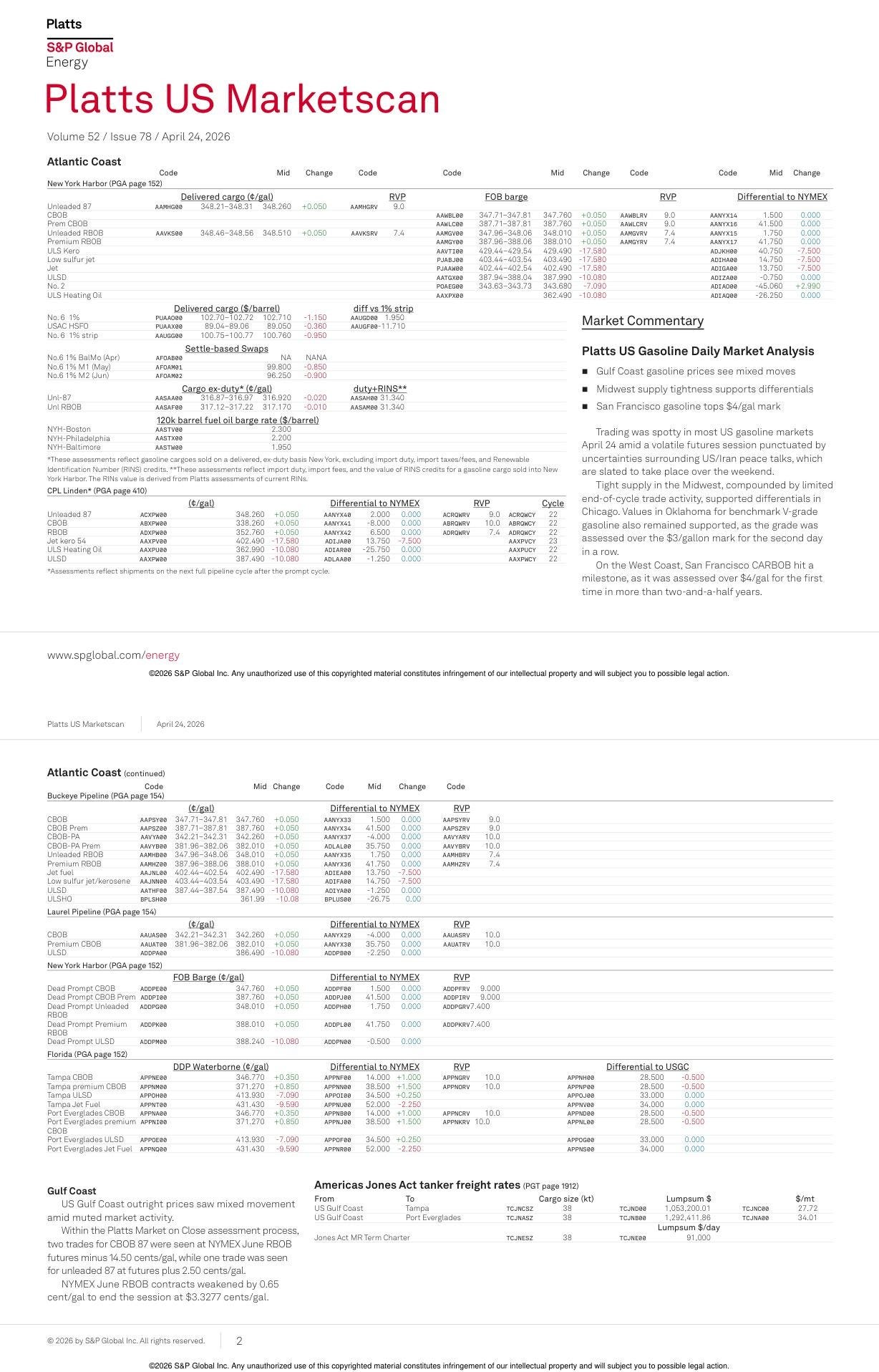

SPREAD-ALARM: Angolan crude in “free fall” The absence of Eastern demand instantly crashed West African differentials:

Nemba FOB Angola, for the first time since March 16, 2023, went to a discount to Dated Brent: minus $0.435/bbl (fall of $3.30 in a day).

Plutonio fell by $2.25/bbl to a premium of $2.45, Pazflor lost $2.175/bbl to a premium of $3.225.

In Platts MOC: Eni offered Nemba 26-27 May at a premium of $3.30, closed without a buyer at a discount of $0.55. ExxonMobil tried to sell Pazflor 29-30 May at a premium of $6, but withdrew the offer at the level of $3. BP offered Plutonio 4-5 June at a premium of $4.75, ending without a deal at $2.50.

According to traders’ estimates, more than 10 May cargoes from Angola and Nigeria remain unplaced, and they are being redirected to Europe. Girassol at the end of May was trading at the level of $3/bbl (against an offer of $4.50 earlier), while the June cargo went for $8+ last week.

“Free fall,” — a third trader characterizes.

North Sea: end of deficit? After several weeks of the most acute supply crunch, the North Sea market sharply weakened:

The physical Dated Brent differential collapsed by 85.5 cents in a day to a premium of $5.035/bbl. This is a fall of 73.85% from the April 13 peak ($19.25/bbl).

Johan Sverdrup FOB Mongstad fell by $2.135 in a day to a premium of $7.15/bbl. Over the week, the grade lost more than $6.

Reason: explosive growth of alternative oil supplies to Europe — the long CPC Blend program, re-offers of West African barrels from Chinese companies, and two VLCCs (2.1 million bbl each) of American Bryan Mound grade from the SPR, heading to the Mediterranean.

Heavyweight traders (Trafigura, Petroineos, Repsol) put up for sale WTI Midland cargoes with delivery in May to Rotterdam. Offers for May 10-14 went at $8.45-$8.60, for May 6-10 — $7.15-$7.30, but no buyers were found. USGC-UKC Aframax freight collapsed to $69.33/t (-56% from April 1).

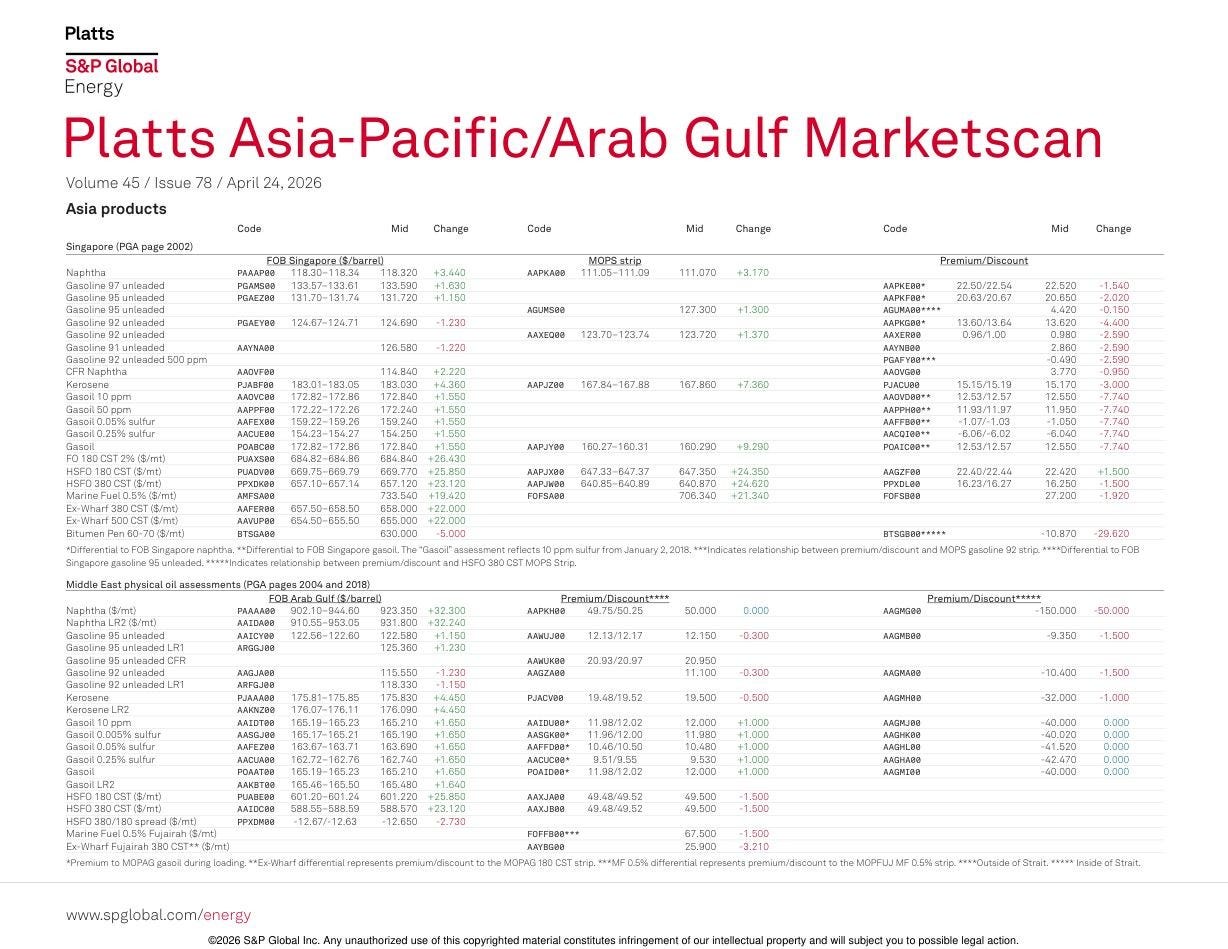

Who buys, who sells Middle East (MOC Singapore, April 24):

Unipec sold 19 June Dubai partial contracts at prices from $106.00 to $107.20/bbl. Buyers: Trafigura, Vitol, BP, Mercuria, TotalEnergies. This is a net volume of 475,000 barrels.

Unipec declared convergence into Oman for Trafigura (20 partial contracts = 500,000 barrels), which speaks to the preservation of physical demand for the grade.

Cash Dubai/Oman/Murban premium decreased by just 4 cents to $11.91/bbl to June Dubai futures. The sour complex is feeling better than sweet against the backdrop of a Middle Eastern barrel deficit.

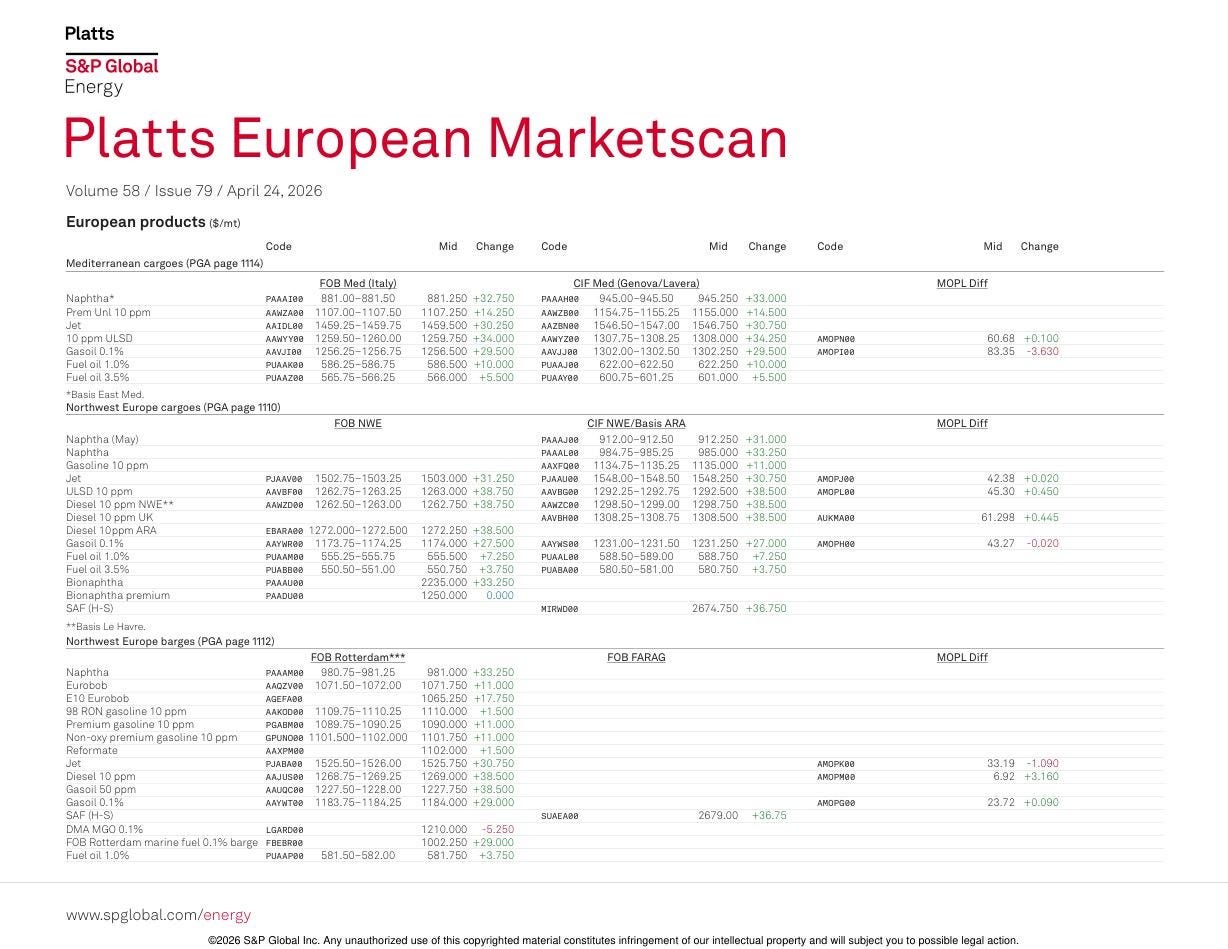

North Sea (MOC London, April 24):

Mercuria was aggressively buying CFDs on Brent, but at the same time selling July Cash BFOE (4 partials were sold at $100.23). Glencore, Trafigura, and Onyx were buying CFD Week 2 (May 11-15) at $6.90, which is lower than previous days. This indicates the hedging of long physical positions and the expectation of further weakening.

BP persistently offered Johan Sverdrup (May 4-6), reducing the price from $11.60 to $9.50, but to no avail.

Conclusion: Large traders are reducing long positions on physical oil in the Atlantic, locking in profits or minimizing losses before the possible opening of the strait.

EN590 / JET A1 / VLSFO: where are the inefficiencies? EN590 (Diesel):

The CIF Med vs CIF NWE spread sharply narrowed from a record $112.25/t to $19.75/t in two days — due to the massive supply of American SPR sour crude and the slowdown of demand in the Mediterranean. But even $19.75 is anomalously wide (in peacetime the spread was $0.25).

ARA stocks fell to a seven-month minimum (1.86 million tons, -11% YoY), despite record supplies from the US. NWE imports in April collapsed by 50.4% compared to January.

The spread between 0.1% and 50 ppm gasoil in ARA turned negative (down to -$65/t). This opens a window for blending: buying cheap high-sulfur gasoil for mixing with expensive ULSD.

JET A1:

The Asian Jet/Kero regrade against 10ppm gasoil collapsed. FOB Singapore cash premium fell to $18.17/bbl (six-week minimum) after South Korean supply (GS Caltex, S-Oil were selling at a premium of $8-9/bbl).

Physical spot in Europe is overheated: ARA stocks at a six-year minimum (579,000 tons, -32% YoY), imports in April fell by >50% YoY. But an LR2 from Oman is already on its way.

VLSFO:

RED III is redrawing the ARA map: sales in Rotterdam fell by 25%, vessels are leaving for Antwerp (growth of 16%). Antwerp’s premium over Rotterdam rose to $23/t.

Singapore Hi-Lo spread (0.5% vs 380 CST) is being maintained at the level of $76.44/t.

DEALS, HEDGING, LOOK AHEAD Indonesia announced plans to purchase 150 million barrels of Russian oil. This is a direct bet on the preservation of Urals with a discount (currently $18.50/bbl to Dated Brent).

US sanctions against Hengli Petrochemical and 38 vessels will sharply reduce Iran’s exports. Exports from Kharg fell to 3 million barrels (against the usual 8 million).

Key risk: if the Pakistani negotiations lead to the opening of Hormuz, the oil curve will crash into contango. Front-month backwardation on Brent (M1-M2) amounts to $6.30/bbl, but may collapse within days. Traders’ actions — aggressive selling of prompt BFOE — is rational hedging.

Final conclusion: The WTI/Brent spread ($10.93), the collapse of Angolan differentials (Nemba at a discount), the anomalous compression of Med/NWE gasoil ($19.75/t) create rare arbitrage windows. The volatility of the Brent structure (a 74% fall in the Dated Brent diff) opens up opportunities for playing the transition from backwardation to contango. History loves the prepared. Good luck!

Based on materials from S&P Global Platts (Oilgram Price Report, US Marketscan, Asia-Pacific/Arab Gulf Marketscan, European Marketscan) of April 23-24, 2026.